Reconciliation Bill of 2025 (One Big Beautiful Bill)

The Reconciliation Bill of 2025 (Public Law 119-21), also referred to as the One Big Beautiful Bill, was signed into law on July 4, 2025. This legislation introduces significant updates to several federal financial aid programs.

To help members of the VCU community understand these upcoming changes, we are sharing our current interpretation of the bill's provisions as they relate to financial aid. Please note that details are still emerging, particularly as the U.S. Department of Education has announced plans to develop new regulations in response to the law. As additional guidance becomes available, we will continue to update this information to reflect the most accurate understanding possible.

Most provisions will take effect beginning with the 2026-27 academic year, though a few exceptions may apply. The contents on this page are provided for informational purposes only and should not be considered official financial or legal advice, as further clarification from federal authorities is expected.

Borrowing

Limits

Federal loans have a lifetime borrowing limit.

Previous Loans Count

Past loans from any school count towards your limits.

Aid May

Change

Your financial aid may be reduced if you're near your limit.

AT A GLANCE: Understanding Your Federal Loan Limits

Federal Student Loan Borrowing Limits

Federal student loans have lifetime borrowing limits, which means there is a maximum total amount you can borrow during your academic career.

These limits include federal loans borrowed:

- At VCU

- At other colleges or universities

- During undergraduate or graduate programs

Why Your Financial Aid May Change

If you are close to or have reached your federal borrowing limit, your financial aid award may be adjusted.

This could result in:

- Reduced loan eligibility

- Updates to your financial aid offer

- A balance due on your student account

Check Your Loan History

Students should regularly review their federal loan history to understand how much borrowing eligibility remains.

You can view your loan history by logging in to studentaid.gov.

Subsidized and unsubsidized aggregate borrowing limits

Subsidized and unsubsidized aggregate borrowing limits for current borrowers:

| Undergraduate Dependent | Undergraduate Independent | Graduate | Professional |

| $31,000 | $57,500 | $138,500 | $224,000 |

Undergraduate federal student loans previously borrowed are included in the aggregate borrowing limits at the graduate and professional school levels. Currently enrolled graduate and professional students must finish their program by July 1, 2029 under these borrowing limit rules.

Subsidized and unsubsidized aggregate and lifetime borrowing limits for new borrowers after July 1, 2026:

| Undergraduate Dependent |

Undergraduate Independent |

Graduate | Professional | Lifetime maximum borrowing all loans |

| $31,000 | $57,500 | $100,000 | $200,000 | $257,500 |

No change to undergraduate aggregate borrowing limits. However, loans at the undergraduate level are not included in the aggregate borrowing limits when determining graduate and professional aggregate loan eligibility for new borrowers. In addition, the total value of all federal student loans borrowed (excluding PLUS loans) cannot exceed $257,500 lifetime from all previous subsidized and unsubsidized loan borrowing.

Professional Degree Programs Defined By The One Big Beautiful Bill Act (OBBBA)

The law defines a professional student as meeting the requirements in Section 668.2 of Title 34 of the Code of Federal Regulations (CFR). The CFR describes professional degree programs as having three defining characteristics:

- Signifies completion of the academic requirements for beginning practice in a given profession;

- Represents a level of professional skill beyond that normally required for a bachelor’s degree; and

- Commonly requires professional licensure after graduation.

Professional programs as defined by the OBBBA are the following:

- Clinical Psychology (Psy.D. or Ph.D.), Pharmacy (Pharm.D.); Dentistry (D.D.S. or D.M.D.); Veterinary Medicine (D.V.M.); Chiropractic (D.C. or D.C.M.), Law (L.L.B. or J.D.);Medicine (M.D.); Optometry (O.D.); Osteopathic Medicine (D.O.); Podiatry (D.P.M., D.P. or Pod.D.); and Theology (M.Div. or M.H.L.).

Update:

The Professional Student Degree Act was introduced in December 2025, to amend the definition of a professional student within the OBBBA, and replace the definition with a more comprehensive list of programs. More information about the introduced legislation can be found here.

Undergraduate Parent PLUS loan annual and lifetime borrowing limits

Undergraduate Parent PLUS loan annual and lifetime borrowing limits for current borrowers:

| Annual Amount A Parent Can Borrow Per Dependent Student | Lifetime Maximum Borrowing All PLUS Loans Per Dependent Student | ||

| No set dollar amount. However, a parent could borrow up to their student's cost of attendance, less all other financial aid offered | No set dollar amount |

Currently enrolled undergraduate students receiving a parent PLUS loan must finish their program by July 1, 2029 under these parent PLUS loan borrowing rules.

Undergraduate Parent PLUS loan annual and lifetime borrowing limits for new borrowers after July 1, 2026:

| Annual Amount A Parent Can Borrow Per Dependent Student | Lifetime Maximum Borrowing All PLUS Loans Per Dependent Student | ||

| $20,000 | $65,000 |

New parent PLUS borrowers can no longer borrow up to their student's cost of attendance starting July 1, 2026. New parent PLUS borrowers will be limited up to $20,000 annually per dependent student and cannot exceed $65,000 lifetime PLUS loan borrowing per dependent student.

Graduate & Professional PLUS loan annual and lifetime borrowing limits

Graduate & Professional PLUS loan annual and lifetime borrowing limits for current borrowers:

| Annual Amount A Student Can Borrow | Lifetime Maximum Borrowing All PLUS Loans | ||

| No set dollar amount. However, a student could borrow up to their cost of attendance, less all other financial aid offered. | No set dollar amount |

Currently enrolled graduate and professional PLUS loan borrowers must finish their program by July 1, 2029 under these PLUS loan borrowing rules.

Graduate & Professional PLUS loan annual and lifetime borrowing limits for new borrowers after July 1, 2026:

| Annual Amount A Student Can Borrow | Lifetime Maximum Borrowing All PLUS Loans | ||

| $0; Program has been eliminated for new borrowers | $0; Program has been eliminated for new borrowers |

Any graduate or professional student who has not previously borrowed a PLUS loan prior to July 1, 2026 is ineligible for PLUS loan borrowing. The One Big Beautiful Bill Act passed by Congress eliminated the PLUS loan program for new graduate and professional PLUS loan borrowers.

Professional Degree Programs Defined By The One Big Beautiful Bill Act (OBBBA)

The law defines a professional student as meeting the requirements in Section 668.2 of Title 34 of the Code of Federal Regulations (CFR). The CFR describes professional degree programs as having three defining characteristics:

- Signifies completion of the academic requirements for beginning practice in a given profession;

- Represents a level of professional skill beyond that normally required for a bachelor’s degree; and

- Commonly requires professional licensure after graduation.

Professional programs as defined by the OBBBA are the following:

- Clinical Psychology (Psy.D. or Ph.D.), Pharmacy (Pharm.D.); Dentistry (D.D.S. or D.M.D.); Veterinary Medicine (D.V.M.); Chiropractic (D.C. or D.C.M.), Law (L.L.B. or J.D.);Medicine (M.D.); Optometry (O.D.); Osteopathic Medicine (D.O.); Podiatry (D.P.M., D.P. or Pod.D.); and Theology (M.Div. or M.H.L.).

Update:

The Professional Student Degree Act was introduced in December 2025, to amend the definition of a professional student within the OBBBA, and replace the definition with a more comprehensive list of programs. More information about the introduced legislation can be found here.

Need help?

Get in touch with a financial counselor:

- Our call center is available 24/7 at (804) 828-1550.

- Office Hours: Monday - Friday: 9 a.m. - 5 p.m.

- Virtual Zoom drop-ins are available Monday through Friday 9 a.m. to 11 a.m. and 2 p.m. to 3:30 p.m.

- Email us at sfmc@vcu.edu

The call center option is provided by Anthology, a secure third-party vendor. Anthology is powered by AI. While Anthology aims to provide accurate information, responses may sometimes contain errors or outdated details. Please double-check information before making important decisions.

Frequently asked questions

Most of the changes go into effect beginning with the 2026-27 school year (as of 7/1/2026), although loan repayment changes have an earlier effective date.

The National Association of Student Financial Aid Administrators (NASFAA) has created a chart that compares current rules (if any) in comparison to the upcoming changes. Keep in mind that some details are still emerging, including the U.S. Department of Education's intent to publish new regulations around these changes in the law. This chart is subject to change as new guidance or rules emerge.

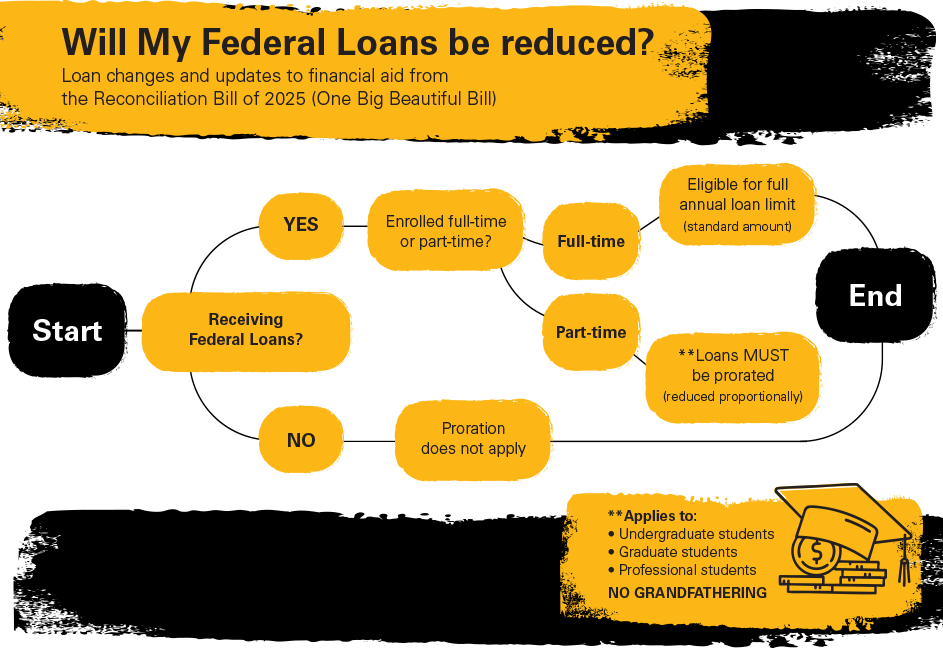

Yes. A legacy provision does exist for three academic years or the remainder of the student's expected time to credential, whichever is less. Note that the legacy provision does not extend to the proration of annual loan amounts for students enrolled less than full-time.

- Graduate PLUS loan: If a borrower has a Federal Direct Loan made before July 1, 2026, while enrolled in a credentialed program, the borrower can borrow from the Graduate PLUS program for three academic years or the remainder of their expected time to credential, whichever is less.

- Parent PLUS loan: If a borrower has a Federal Direct Loan made before July 1, 2026, while the dependent student is enrolled in a credentialed program, the parent can borrow under current loan limits for three academic years or the remainder of their dependent student's expected time to credential, whichever is less.

- Graduate/professional annual and aggregate loan limits: If a borrower has a Federal Direct Loan made before July 1, 2026, while enrolled in a credentialed program, the borrower can continue to borrow under current limits for three academic years or the remainder of their expected time to credential, whichever is less.

- Federal Loan Program lifetime loan limits: If a borrower has a Federal Direct Loan made before July 1, 2026, while enrolled in a credentialed program, the borrower can continue to borrow under current loan limits for three academic years or the remainder of their expected time to credential, whichever is less.

- Annual borrowing limits (Subsidized and Unsubsidized Loans):

- Undergraduate students: No change (Subsidized and Unsubsidized)

- Graduate students: No change (Unsubsidized)

- Professional students: Increased annual limit (Unsubsidized)

- Aggregate borrowing limits:

- Undergraduate students: No change (Subsidized and Unsubsidized)

- Graduate students: Reduced aggregate limit, but will exclude from aggregate any amounts borrowed at the undergraduate level

- Professional students: Increased aggregate limit, and will exclude from aggregate any amount borrowed at the undergraduate level

- Lifetime borrowing limit:

- All students: New lifetime borrowing limit across all federal student loan programs (Subsidized, Unsubsidized, and Graduate PLUS), but excludes Parent PLUS borrowing that occurred on the student's behalf

- Parent PLUS loan limits (loan program for parent(s) of dependent undergraduate students)

- New annual cap of $20,000 per dependent student (combined across all parents borrowing that year for the dependent student; previously no limit other than Title IV cost of attendance minus all other aid offered/received)

- New aggregate limit of $65,000 per dependent student (combined across all parents borrowing Parent PLUS for the student); previously no aggregate limit

- Graduate PLUS loan program eliminated

Students may review alternative/private education loan options using ELMSelect.

Students may consider applying for available department and donor scholarships through the Ram Scholarship Hub and/or external scholarships. VCU also offers an Installment Payment Plan that allows students to divide the cost of tuition, fees, dining and housing plans into four installment payments throughout the semester.